Warnings that next PMI survey will start to see impact of former prime minister’s mini-budget debacle

UK industry activity grew last month at its fastest pace since May despite growth expectations among construction firms remaining subdued.

Optimism fell sharply to its lowest point in almost two and a half years, reflecting falling volumes of new work and broader concerns about the state of the economy.

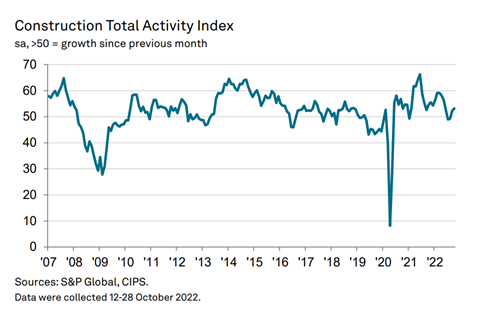

According to the latest PMI data, the index recorded a reading of 53.2 in October, up from 52.3 in September and attributed to a combination of new project starts and strong pipelines of unfinished work.

It comes after the Bank of England yesterday raised interest rates to 3%, their highest level since 2008, and warned the UK economy is entering a two-year recession, the worst since the 1920s.

Tim Moore, economics director at S&P Global Market Intelligence, which compiles the survey, said forward-looking survey indicators suggested growth would be “harder to achieve in the coming months” in the wake of September’s abandoned mini-budget as rising borrowing costs, economic uncertainty and cost constraints hit order books in October.

Moore said business optimism was “by far the weakest since the early pandemic months”, with 33% of the survey panel anticipating a rise in activity and 26% predicting a decline.

“Construction firms cited concerns about a broad-based decline in client demand due to cutbacks on non-essential spending among clients, although some noted that growth linked to green energy projects, planned infrastructure spending and success in niche markets could help to offset the UK economic headwinds,” he added.

The finance director of regional contractor, Fraser Johns, said: “With the higher cost to borrow and tighter access to credit, it doesn’t come as a surprise to see a drop in confidence or the number of new orders.”

Commercial building was the best performing category (54.5), with output reaching a five-month high, while residential grew at a softer rate (51.2). Civils work decreased for the fourth month running (48.5).

The survey reported an easing of supply chain pressures, though cost burdens across the sector continue to rise due to greater energy costs.

Max Jones, director in Lloyds Bank’s infrastructure and construction team, said: “Contractors have had some respite on the materials inflation front, with prices easing back in recent months. But challenges remain on salaries, which will make recruiting and retaining talent tricky in the near term.”

>> Latest trends and prices data dashboard

And Mark Robinson, group chief executive at procurement authority Scape, said construction growth “continues to fly in the face of wider market conditions”.

“Looking ahead, firms will have one eye on the upcoming Autumn Statement [on 17 November] and its impact on the public purse – which often supports development activity during economic downturns,” he said.

No comments yet